In this Edition:

INFLATION RESURGENCE WEIGHS ON US MARKET SENTIMENT

US inflation rose again, while retail sales and changes in Fed leadership kept policy expectations in focus.

EUROPEAN DATA SOFTENS AS POLITICAL UNCERTAINTY RISES

Eurozone production missed expectations and UK political uncertainty intensified.

ASIA WEAKENS AS YEN PRESSURE OFFSETS STRONGER CHINA SERVICES DATA

Asian markets softened despite stronger Chinese services data and renewed US-China dialogue.

SOUTH AFRICAN INDUSTRIAL RESILIENCE OFFSETS WEAKER RISK SENTIMENT

Local industrial data improved, but equities and the rand weakened.

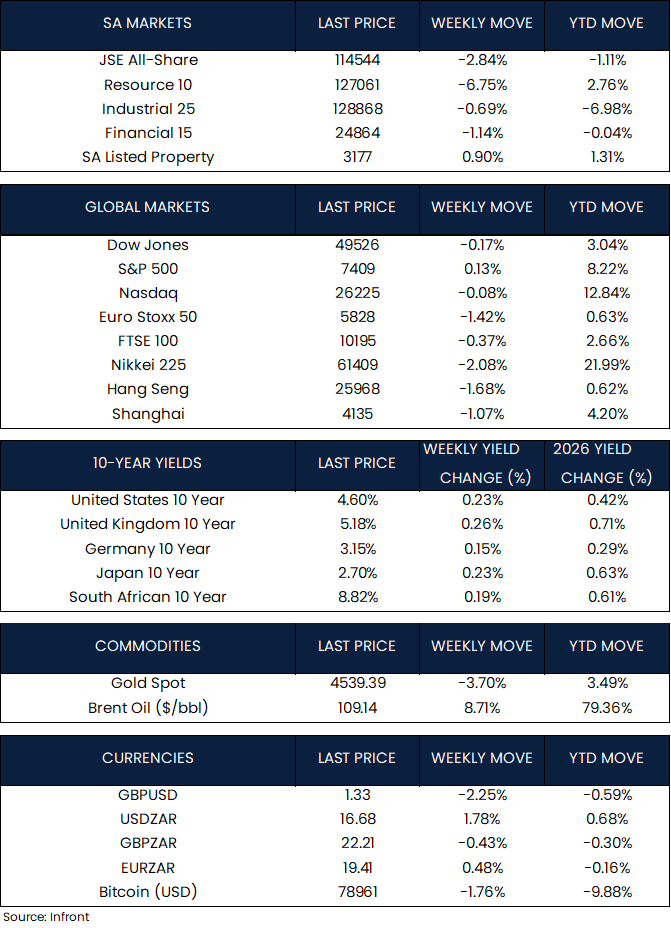

MARKET MOVES OF THE WEEK

Source: Infront (16 May 2026)

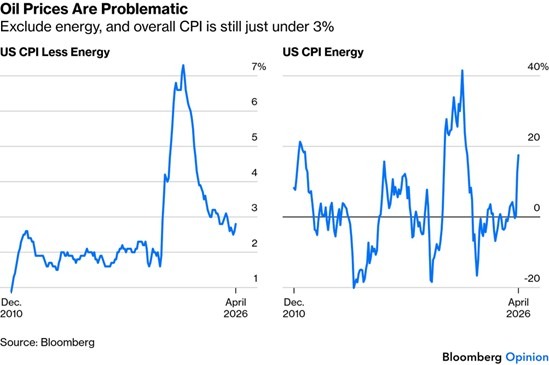

CHART OF THE WEEK

Source: Bloomberg (16 May 2026)

U.S. headline inflation accelerated to 3.8% in April, the highest level since May 2023, as rising energy prices linked to disruptions around the Strait of Hormuz continued to place upward pressure on consumer prices. In contrast, core inflation remained relatively more contained at 2.8%, suggesting underlying inflationary pressures were less severe outside of energy-related components.

Inflation resurgence weighs on US market sentiment

According to data released by the U.S. Bureau of Labor Statistics (BLS), U.S. inflation remained elevated in April. Headline CPI rose 0.6% month-on-month, while annual inflation accelerated to 3.8%, the highest level since May 2023, driven largely by higher energy prices. Core CPI also surprised slightly to the upside, increasing 0.4% month-on-month and 2.8% year-on-year, reinforcing concerns around persistent underlying price pressures.

Producer price data released later in last week by the BLS added to the inflationary backdrop, with PPI rising 1.4% in April and annual producer inflation accelerating to 6.0%, supported again by higher energy costs.

Meanwhile, the U.S. Census Bureau reported that U.S. retail sales increased 0.5% in April, moderating from March’s revised 1.6% gain but remaining broadly in line with expectations. Excluding autos, sales rose 0.7%, while the control group measure, which feeds into GDP calculations, increased 0.5%. Gains were driven mainly by gas stations, sporting goods and hobby stores, and electronics retailers.

Kevin Warsh was confirmed by the Senate as the next Chair of the Federal Reserve, replacing Jerome Powell following the expiry of his term on 14 May. Powell will remain on the Fed’s board as a governor, while Warsh is expected to be formally sworn in ahead of the next FOMC meeting in June.

Most major U.S. equity indices ended the last week broadly weaker as optimism around large-cap technology and artificial intelligence (AI)-related stocks was offset by concerns over persistent inflation, higher Treasury yields, elevated oil prices, and ongoing geopolitical uncertainty. The Dow Jones Industrial Average declined 0.17% over the last week, while the Nasdaq fell 0.08%. In contrast, the S&P 500 posted a modest gain of 0.13%.

European data softens as political uncertainty rises

In Europe, eurozone industrial production rose 0.2% month-on-month in March, slightly below expectations. Growth was supported by intermediate and capital goods production, while energy and non-durable consumer goods output declined. Industrial production weakened in Germany, while France, Italy, and Spain recorded increases.

In the UK, political uncertainty intensified as Prime Minister Keir Starmer faced mounting pressure following a series of ministerial resignations, while speculation around a potential leadership challenge from Andy Burnham added to uncertainty around the future direction of the Labour Party.

European equities also weakened, with the Euro Stoxx 50 Index declining 1.42% and the UK’s FTSE 100 Index falling 0.37%.

Asia weakens as yen pressure offsets stronger China services data

The Japanese yen weakened to around JPY 158 against the U.S. dollar, from JPY 156.6 at the end of the week before last, as the impact of suspected intervention by Japanese authorities appeared short-lived. Market focus remained on the policy divergence between the Federal Reserve and the Bank of Japan, while U.S. officials reiterated that excessive currency volatility is undesirable.

In China, the services sector activity expanded at a stronger-than-expected pace in April, with the RatingDog China General Services PMI rising to 52.6 and the composite PMI output index increasing to 53.1. S&P Global noted that the improvement was driven mainly by stronger domestic demand and firmer new business growth despite softer export orders.

Meanwhile, U.S. President Donald Trump and Chinese President Xi Jinping held a two-day summit in Beijing, where discussions centred on maintaining stable bilateral relations and avoiding a renewed escalation in trade tensions. Talks included potential increases in Chinese purchases of U.S. agricultural and energy products, market access for U.S. businesses, and mechanisms to manage disputes around semiconductors and rare-earth supply chains, although no meaningful easing of export restrictions was announced. Taiwan also remained a key issue, with Xi warning that mishandling the matter could damage broader relations between the two countries.

In Japan, the Nikkei 225 Index declined 2.08%, while Chinese equities ended lower after earlier gains faded later in the week, with the Shanghai Composite Index falling 1.07% and the Hang Seng Index declining 1.68%.

South African industrial resilience offsets weaker risk sentiment

In South Africa, mining production rose 2.5% year-on-year in March, slowing from February’s revised 9.7% increase and coming in below expectations, as weaker coal and iron ore output weighed on overall production. The data nonetheless pointed to continued resilience in parts of the sector amid a still-supportive commodity price environment.

Meanwhile, manufacturing production increased 0.9% year-on-year in March, rebounding from weakness earlier in the year and supported by stronger activity in the food, petroleum, and motor vehicle sectors. The release added to signs that domestic industrial activity may be stabilising despite ongoing logistical and cost pressures.

South African markets ended last week lower, with the JSE All Share Index declining 2.84% amid weaker global risk sentiment and higher oil prices. The Resource 10 Index led losses, falling 6.75%, while the Financial 15 and Industrial 25 indices declined 1.14% and 0.69%, respectively. In contrast, listed property outperformed, with the SA Listed Property Index gaining 0.90% over the last week. Meanwhile, the rand weakened 1.78% against the U.S. dollar to 16.68/USD.

The information contained in this recording/presentation is for general information purposes only and should not be construed as, nor does it constitute financial, tax, legal, investment or any other advice. Carrick does not guarantee the suitability or potential value of any products or investments discussed herein. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability or availability with respect to the information, products, services, or any other content contained in this recording for any purpose. Carrick accepts no responsibility for the suitability or accuracy of the information or for any errors or omissions that may occur. Therefore, any reliance you place on such information is strictly at your own risk. This material is provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although Carrick does not represent this as accurate or complete and it shouldn’t be relied upon as such. All material, content, and information provided by Carrick is the intellectual property of Carrick Group and its affiliates, unless otherwise stated. No part of this material may be copied, reproduced, distributed, published, or used for any commercial purpose without Carrick’s prior written consent, and is provided solely for non-commercial use. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting an investment.